RBC Says The Omicron Spread to Pause Canada’s Economic Recovery

From – tradingview.comJanuary 10, 2022. MT Newswires

RBC said that a quiet macroeconomic economic calendar for Canada this week will keep the focus on COVID-19 developments.

Canadian provincial governments havd re-introduced measures to slow the pandemic spread, including mandated closures of high-contact services like restaurant dining rooms and gyms in Ontario and Quebec. the bank expected businesses within the travel and hospitality sectors to continue to bear the brunt of restrictions.

Indeed, RBC card spending data already indicated a sharp decline in travel spending in December. And the exceptionally high rate of omicron spread had probably pushed a large share of the Canadian workforce into self-isolation, adding to near-term labor supply issues in other sectors.

All told, the bank predicted Q1 gross domestic product (GDP) to look decidedly softer and had revised its growth projection to 1.5% from 4% for the quarter. With testing capacity overwhelmed in many regions, hospitalization rates will be carefully scrutinized for a sense of how quickly restrictions could be eased.

This latest wave of COVID-19 was multiples larger than those that preceded it, added RBC. But the speed of the spread meant it was also expected to run its course more quickly, the bank estimated growth in the economy to bounce back in Q2.

RBC didn’t forecast the latest wave of virus spread to prevent the United States Federal Reserve or the Bank of Canada (BoC) from hiking interest rates in the first half of this year.

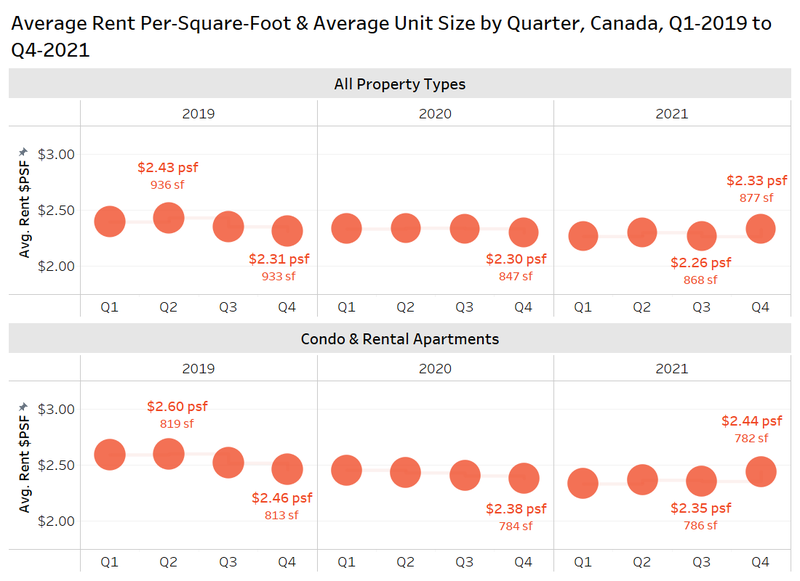

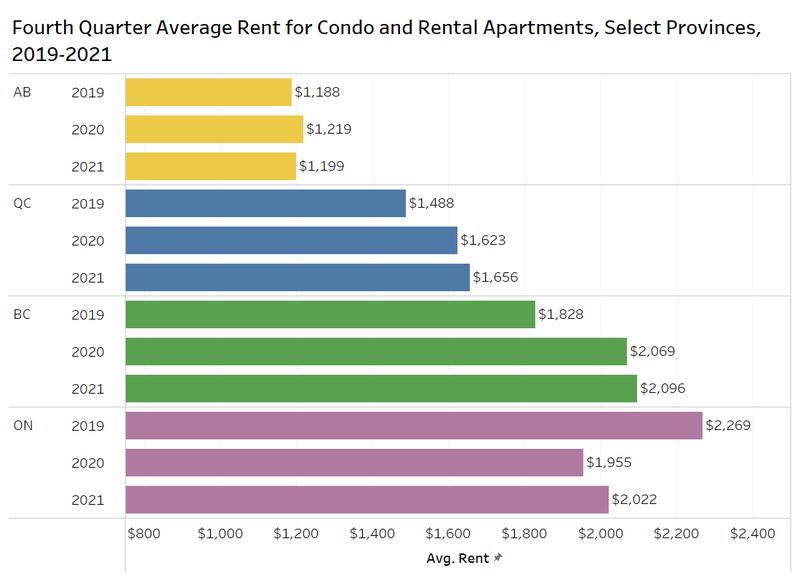

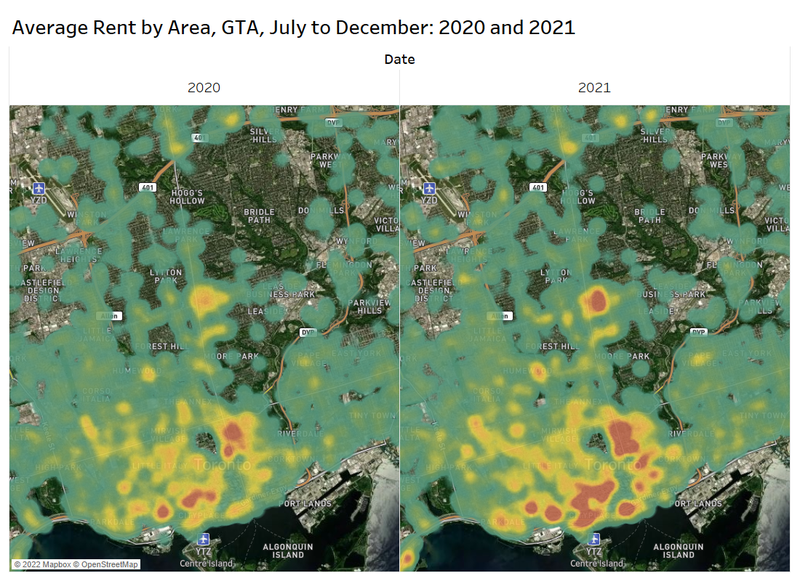

Average rents in Canada up annually, according to report, while Greater Sudbury’s down year over year

From thesudburystar.com.

January 18, 2022. Sudbury Star Staff.

PHOTO BY GETTY IMAGES

While the average rent in Canada was up year over year in December, that wasn’t the case in Greater Sudbury, according to latest National Rent Report by Rentals.ca and Bullpen Research and Consulting .

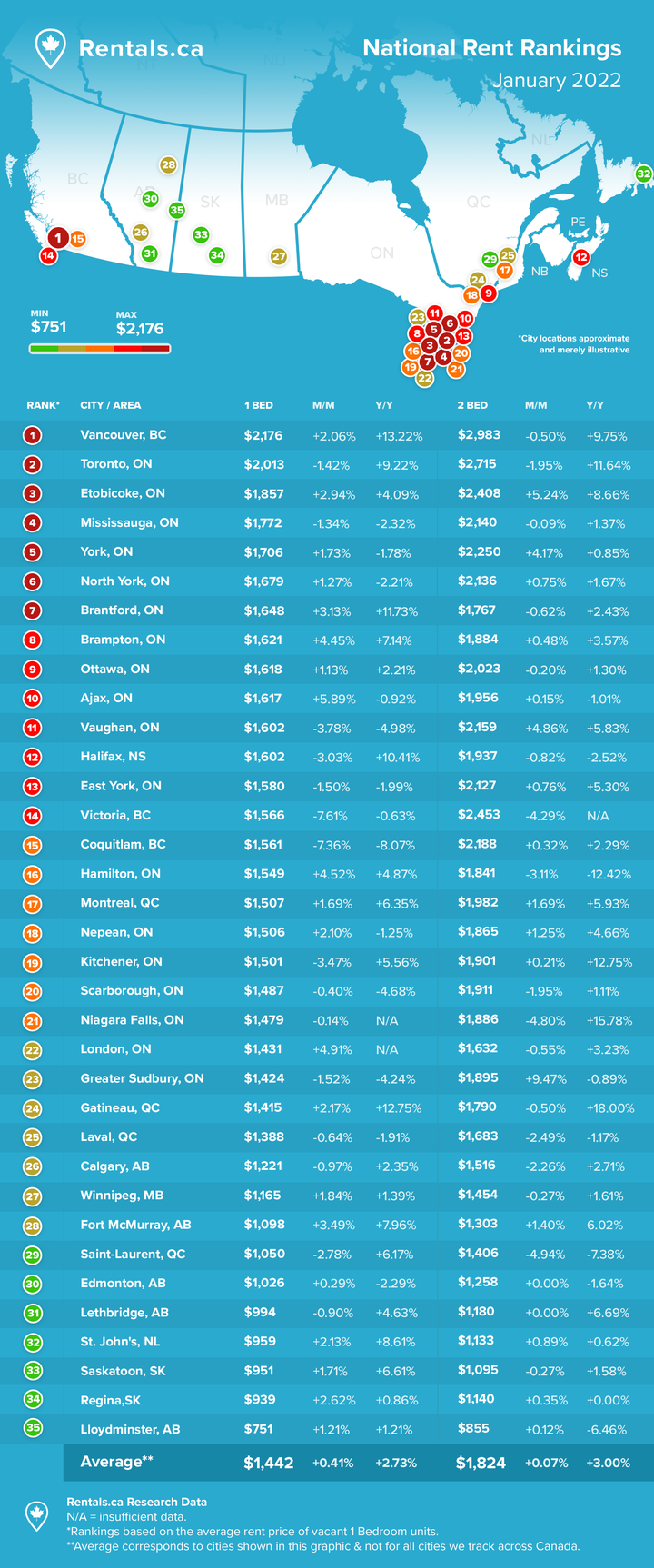

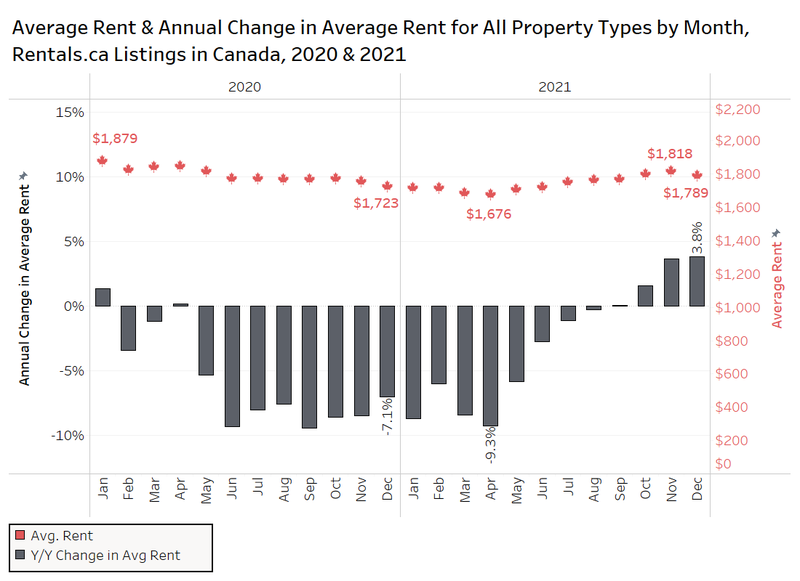

The average rent for all Canadian properties last month was $1,789 per month, up 3.8 per cent annually, according to the report. December was the fourth consecutive month average asking rents were positive year over year based on Rentals.ca listings, following 16 consecutive months of annual decline.

For the first time since April, the average rent decreased month over month, falling 1.5 per cent from $1,818 per month in November.

Greater Sudbury finished 23rd on the list of 35 cities for average monthly rent in December for a one-bedroom, at $1,424, and 17th for a two-bedroom, at $1,895.

Year over year, average monthly rents in the city declined in December by 4.2 per cent for a one-bedroom and 0.9 per cent for a two-bedroom.

Ontario’s rent for all property types increased annually by 5.4 per cent to $2,087 per month in the fourth quarter of 2021, compared to the fourth quarter of 2020.

Rental rates tend to fall in December, as prospective tenants concentrate on the holidays, rather than looking for apartments. It is not likely that the Omicron variant of the COVID-19 virus was a major factor, the report authors said, as average rents declined 1.8 per cent monthly in December 2020, and 3.3 per cent monthly in December 2019.

“Average rental rates moderated in December after rents surged following the April market bottom, where rents had fallen by over nine per cent annually,” Ben Myers, president of Bullpen Research and Consulting, said in a release. “It is too early to tell if Omicron will have a prolonged deflationary impact on the rental market, but Bullpen Research and Consulting and Rentals.ca still believe there will be significant upward growth in rents in 2022 in Canada’s major markets.”

Although the real estate market has recovered in the last several months, the report authors said uncertainty will persist as governments issue further lockdown measures because of the Omicron variant, but there is some consensus among experts that these lockdowns and restrictions will be much shorter than previous ones, so the Bullpen Research and Consulting/Rentals.ca forecast of continued rent growth in most major markets in 2022 has not been altered.

The rental market in Canada is returning to levels seen at the start of 2020, the report said, but remains $165 below the peak average rent of $1,954 in September 2019.

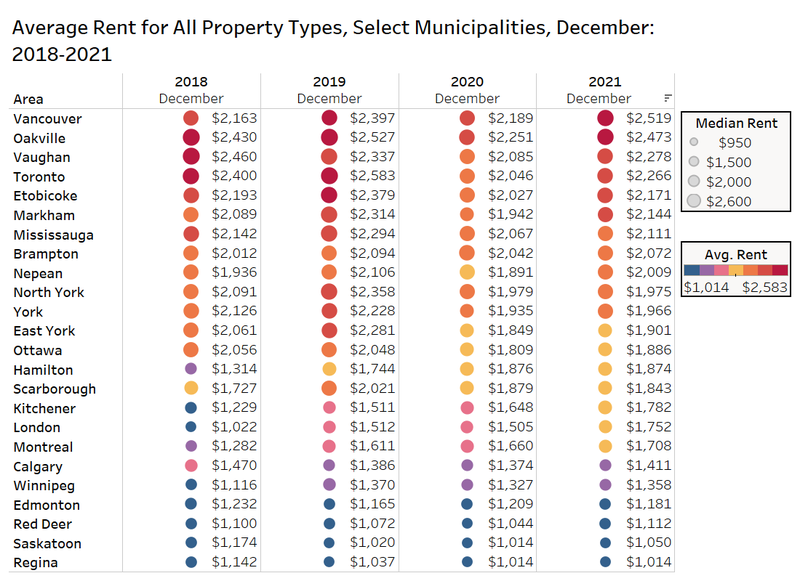

Vancouver topped the list of 35 cities for average monthly rent in December for a one-bedroom home, at $2,176, and for average monthly rent for a two-bedroom, at $2,983.

Toronto finished second on the list of 35 cities for average monthly rent in December for a one-bedroom, at $2,013, and for a two-bedroom, at $2,715.

Montreal came in 17th for average monthly rent in December for a one-bedroom home, at $1,507, and 12th for average monthly rent for a two-bedroom, at $1,982.

The majority of municipalities in the chart below saw an increase in average rent, according to the report, from December 2020 to December 2021. North York, Scarborough, Hamilton, and Edmonton were the only municipalities that experienced a small decline in average rent.

Vancouver had the highest average rent in December among the municipalities and former municipalities, at $2,519 per month, an annual increase of 15 per cent from the December 2020 average of $2,189 per month. Oakville had the next highest average rent at $2,473 per month — an annual increase of 9.9 per cent from its December 2020 average of $2,251 per month.

Toronto average rent increased from $2,046 in December 2020 to $2,266 this December; Ottawa average rents went from $1,809 to $1,886; London average rents increased to $1,752 in December from $1,505 a year earlier; Montreal average rents rose to $1,708 from $1,660; while Calgary, Winnipeg and Saskatoon average rents were up slightly year over year.

Regina had the lowest average rent out of the municipalities with an average of $1,014 per month, unchanged from the previous year.

The Bullpen Research and Consulting and Rentals.ca forecasts for the rental market in 2021 were fairly close for Calgary, Mississauga, Montreal, and Toronto, with average rents in the select municipalities landing within $150 of the averages forecasted. The average rent in Vancouver at $2,519 per month in December 2021 was much higher than the predicted average of $2,240 per month.

“December is typically one of the slowest months for rental activity every year, and 2021 appears to be no exception,” Myers said.

The National Rent Report charts and analyzes monthly, quarterly and annual rates and trends in the rental market on a national, provincial, and municipal level across all listings on Rentals.ca for Canada.

Investors and repeat buyers make up growing share of Canadian real estate market: study

From ctvnews.caBy Ian Holliday – January 16, 2022

B.C. saw a record number of new homes registered for construction in 2021, but data from the Bank of Canada suggests a significant share of them are likely to be purchased by investors.

The Bank of Canada study looked at mortgage and credit bureau data to determine the percentage of homes in the country being purchased by first-time homebuyers, repeat buyers and investors.

It concluded that investors and repeat buyers make up an increasingly large portion of mortgage-backed home purchases in Canada.

“Home purchases are being driven increasingly by existing homeowners,” the study’s authors write in their conclusion.

“Within this group, investors have seen the largest gain in their share of home purchases during the COVID 19 pandemic.”

Because the study looked at mortgage data, it does not capture homes purchased in cash or by corporations, according to the authors.

The study found first-time buyers made up 47 per cent of the market as of June 1, 2021, down from 53 per cent at the start of 2015.

Meanwhile, the percentage of repeat buyers and investors in the market have both increased. In the study, “repeat buyers” are those who are buying a new home and selling their old one, while “investors” are those who are purchasing a new home and holding onto their old one, often with the goal of renting out one of the properties as a source of income.

Repeat buyers were 33 per cent of the market as of June 2021, up from 30 per cent in January 2015, and investors made up 21 per cent of the market, up from 18 per cent.

During the COVID-19 pandemic, as home sales and prices skyrocketed, purchases by investors grew the most. Investors purchased twice as many homes in June 2021 as they did in June 2020, a 100 per cent increase in the number of purchases.

For repeat buyers, the increase over the same period was 66 per cent, while first time buyers’ purchases grew by 47 per cent.

The Bank of Canada study was published the same week the B.C. government touted a record number of new home registrations in 2021.

“Registered new homes data is collected at the beginning of a project, before building permits are issued, making it a leading indicator of housing activity in B.C.,” the province said in a news release.

The latest numbers from BC Housing show 53,189 new homes were registered in B.C. in 2021. That’s a 67.5 per cent increase from 2020 and the highest yearly total since the provincial housing authority began collecting data on new home registrations in 2002.

The total includes 12,899 purpose-built rentals, a 47.7 per cent increase from the previous year.

“This report shows that we can meet the challenge to increase the supply of desperately needed rental homes for individuals, families and seniors in B.C., if cities partner with us to get building permits issued quickly for these registered units,” said David Eby, B.C.’s Attorney General and Minister Responsible for Housing, in the province’s release.

B.C. saw a record number of new homes registered for construction in 2021, but data from the Bank of Canada suggests a significant share of them are likely to be purchased by investors.

The Bank of Canada study looked at mortgage and credit bureau data to determine the percentage of homes in the country being purchased by first-time homebuyers, repeat buyers and investors.

It concluded that investors and repeat buyers make up an increasingly large portion of mortgage-backed home purchases in Canada.

“Home purchases are being driven increasingly by existing homeowners,” the study’s authors write in their conclusion.

“Within this group, investors have seen the largest gain in their share of home purchases during the COVID 19 pandemic.”

Because the study looked at mortgage data, it does not capture homes purchased in cash or by corporations, according to the authors.

The study found first-time buyers made up 47 per cent of the market as of June 1, 2021, down from 53 per cent at the start of 2015.

Meanwhile, the percentage of repeat buyers and investors in the market have both increased. In the study, “repeat buyers” are those who are buying a new home and selling their old one, while “investors” are those who are purchasing a new home and holding onto their old one, often with the goal of renting out one of the properties as a source of income.

Repeat buyers were 33 per cent of the market as of June 2021, up from 30 per cent in January 2015, and investors made up 21 per cent of the market, up from 18 per cent.

During the COVID-19 pandemic, as home sales and prices skyrocketed, purchases by investors grew the most. Investors purchased twice as many homes in June 2021 as they did in June 2020, a 100 per cent increase in the number of purchases.

For repeat buyers, the increase over the same period was 66 per cent, while first time buyers’ purchases grew by 47 per cent.

The Bank of Canada study was published the same week the B.C. government touted a record number of new home registrations in 2021.

“Registered new homes data is collected at the beginning of a project, before building permits are issued, making it a leading indicator of housing activity in B.C.,” the province said in a news release.

The latest numbers from BC Housing show 53,189 new homes were registered in B.C. in 2021. That’s a 67.5 per cent increase from 2020 and the highest yearly total since the provincial housing authority began collecting data on new home registrations in 2002.

The total includes 12,899 purpose-built rentals, a 47.7 per cent increase from the previous year.

“This report shows that we can meet the challenge to increase the supply of desperately needed rental homes for individuals, families and seniors in B.C., if cities partner with us to get building permits issued quickly for these registered units,” said David Eby, B.C.’s Attorney General and Minister Responsible for Housing, in the province’s release.

“The numbers show that together we can respond to the more than 25,000 new people who moved to British Columbia in the last three months looking for homes, and the thousands more who we know are still coming,” Eby added. “We can only succeed in this major challenge if we have committed partners in cities, the federal government, non-profits, First Nations and the private sector to get these registered homes built and open.”

The majority of the newly registered homes are not rentals, however, and the Bank of Canada data suggests a substantial number of them will be bought by investors, as B.C.’s real estate market continues to spiral out of reach of many would-be first-time buyers.

In an interview earlier this month, UBC director of urban economics and real estate Thomas Davidoff told CTV News current conditions benefit people who already own property, rather than those trying to get into the market.

“If we persist in having an environment with very low interest rates and very high rent growth, then yeah I think it’s going to get harder and harder for people to accumulate down payments and really be able to amortize mortgages over their working life,” Davidoff said.

GTA home prices still forecast to rise 11 per cent in 2022 even with expected interest rate hikes: Royal LePage

From cp24.comBy Chris Fox – January 14, 2022A real estate sold sign is shown in a Toronto west end neighbourhood May 17, 2020. THE CANADIAN PRESS/Graeme Roy

Real estate brokerage Royal LePage says that the expected rise in interest rates in 2022 “may not be enough tooffset the significant upward price pressure” on homes, especially in the Greater Toronto Area where it expects the cost of the average property to go up by double-digits once again.

The brokerage said that the aggregate price of a home in the Greater Toronto Area increased by 17.3 per cent in 2021 to $1,119,800 as demand continued to outpace supply.

It is forecasting that in 2022 prices in the GTA will rise by another 11 per cent, with the aggregate home price reaching $1,243,000 by the fourth quarter.

The forecasted price growth comes despite market expectations that the Bank of Canada could raise interest rates up to five times in 2022, significantly increasing the cost of borrowing.

“It isn’t sustainable. The good news, if you could call it that, is we see all prices rising at about half the rate they did in 2021 in the months ahead so while home prices continue to be more expensive the rate at which they’re getting more expensive is falling,” Royal LePage President and CEO Phil Soper told CP24 on Friday morning. “We will find things return to normal appreciation levels sometime in the future, my guess is by 2023 we will be back into single-digit increases, which is what we have come to expect in the city and across the country over the decades.”

The Bank of Canada’s overnight lending rate has been at its effective lower bound of 0.25 since early on in the COVID-19 pandemic but with inflation surging and employment numbers back to their pre-pandemic norms the central bank is expected to begin a cycle of rate hikes in the coming months.

Soper said that when that happens it will effectively make homes more expensive and “some people will get priced out of the market.”

But he said that it likely won’t be enough to tame rising housing prices, given the lack of supply.

“We’ve been building to this lack of supply for years unfortunately and it really came to a head during the pandemic when there was such hyper focus on our homes,” he said. “People were saving money. They were not travelling, they weren’t going out to restaurants and they redirected that money, a lot of it, into their living conditions.”

Royal LePage says that in 2021 the median price of a detached home in the Greater Toronto Area increased 22.4 per cent to $1,421,200 while the median price of a condominium increased 14.8 per cent to $665,400.

Soper, however, said that price growth in condos could outpace detached homes in 2022 due to the “growing gap” in prices, at least in the GTA.

Jobs recovery bolsters case for Bank of Canada to hike soon.

55,000 job gains put employment back to where it would have been if the pandemic crash hadn’t happened.Kevin Carmichael – January 7, 2022Statistics Canada says the economy added 55,000 jobs in December. PHOTO BY JOE RAEDLE/GETTY IMAGESThe “complete” recovery from the COVID-19 recession that Bank of Canada governor Tiff Macklem said he wanted to orchestrate is within view, meaning the time for ultra-low interest rates is over.

Employers created another 55,000 positions in December, putting total employment back to where it would have been if the trend hadn’t been interrupted by an epic economic collapse in March 2020, according to data released by Statistics Canada on Jan. 7.

The jobless rate dropped to 5.9 per cent, somewhat higher than before the pandemic, but now comfortably in a zone many economists associate with full employment.

Macklem has spent the past 18 months explaining that the labour market is too complex to be summed up by those two headline figures. He and his deputies have been using an array of more granular indicators to obtain a more qualitative assessment of the strength of the labour market.

The United States Federal Reserve introduced a similar methodology in the aftermath of the Great Recession, discovering it could keep interest rates lower than it had previously thought without stoking inflation.

“Traditional labour market indicators, such as the unemployment rate, did not fully capture the experiences of different workers over the course of the pandemic,” Lawrence Schembri, a deputy governor, said in a speech on Nov. 16. “The persistence of this uneven impact over the past year and a half has highlighted the need to develop an expanded and integrated set of labour market indicators.”

Many of those indicators are now back at pre-pandemic levels, enhancing the case for an interest-rate increase soon, perhaps even at the end of January when policy-makers next gather to update their assessment of the economy and recalibrate policy.

The latest wave of COVID-19 infections will give them pause. But whereas the Great Recession was followed by a long period of disappointing economic growth, the recovery from the pandemic-driven recession has stoked worrying levels of inflation around the world.

The index Statistics Canada uses to track prices of raw materials surged 36.2 per cent in November from a year earlier, while its index of prices for industrial products increased 18 per cent over the same period.

It’s reasonable to assume a significant portion of the population is as concerned about the cost of living as it is about the pandemic. Bloomberg News reported this week that almost nine in 10 respondents to a poll by Nanos Research said they are more worried about the current pace of rising prices than they are about higher interest rates.

That suggests most people feel good about their prospects. The December hiring data show why that’s probably the case. Statistics Canada’s “underutilization rate,” a gauge Macklem has said he’s watching particularly closely, dropped to 12 per cent last month, the lowest since the start of the pandemic.The figure — which measures the proportion of people in the potential labour force who are unemployed, want a job but have not looked for one, or are employed but working less than half their usual hours — was 11.4 per cent in February 2020. However, Statistics Canada noted the pre-pandemic reading was unusually low, since monthly rates ranged from 11.5 per cent to 12.2 per cent in 2018 and 2019.

“With labour markets expected to bounce back relatively quickly, and inflation pressures continuing to intensify, the latest pandemic disruptions aren’t expected to prevent the Bank of Canada from kicking off a rate-hiking cycle,” said Nathan Janzen, an economist at Royal Bank of Canada.

The participation rate — the percentage of the population aged 15 and older that is working or looking for work — was 65.3 per cent in December, matching its pre-pandemic level. The participation rate of the “core” working population, which Statistics Canada defines as people who are between 25 and 54 years old, was a record 88.3 per cent.

Subsets of the labour market that were disproportionately sidelined during the early stages of the recession, including women and Indigenous workers, have now recovered, according to the latest hiring data. Full-time employment is leading the charge, further evidence the economy has returned to a solid footing.

To be sure, the employment numbers are about to experience a setback. Statistics Canada’s latest Labour Force Survey was completed before Quebec, Ontario and other provinces initiated new health restrictions to slow the spread of the Omicron variant. Anecdotal evidence of a COVID-19-induced soft patch could prompt the Bank of Canada to leave interest rates unchanged at its Jan. 26 policy announcement.

“Without Omicron, the Bank of Canada would have likely had the green light to start raising interest rates at its January 26 meeting,” Sébastien Lavoie, chief economist at Laurentian Bank Securities and a former Bank of Canada staffer, said in a note to his clients. “But given the current wave and its negative impact on workers in services industries, and that (gross domestic product) should contract moderately in January, it appears difficult from a communication standpoint to justify a policy hike as soon as this month.”

The next scheduled opportunities to raise interest rates for the first time since the start of the pandemic would be March 2 and April 13.

Lavoie said he thinks Macklem will wait until April, but acknowledged March is definitely possible. The Canadian economy is getting better at pushing through waves of COVID-19 infections, so there is little reason to bet that the pandemic will knock the Bank of Canada off its course to remove stimulus as soon as possible. The data argue against Here.

Economists forecast rising home sales, prices in 2022.

CIBC is the outlier in forecasting a national 15% drop in sales compared with 2021

January 10, 2022Despite headwinds, most analysts forecast robust housing market this year | Photo: Rob KruytMost of Canada’s biggest mortgage lenders and its largest real estate groups are forecasting a robust housing market this year, with some expecting double-digit sale increases and sharp price hikes, despite rising lending rates and a shortage of homes for sale.

CIBC, however, believes overall residential sales will decline this year, though condo prices could rise.

And the BC Real Estate Association sees the provincial sales pace slowing, with a 15% decline in home transactions in 2022, compared with the record-setting pace of 2021.

The outlook from most analysts parallels that of the Canadian Real Estate Association, which expects 2022 home sales to increase 8.6% compared with last year, with prices rising 7.6%.

Royal LePage, citing rising immigration, predicts that average house prices will increase 10.5% in 2022. Re/Max Canada sees a 9.2% price increase, year-over-year.

All the forecasts, however, are shadowed by the fact that most analysts expect the Bank of Canada overnight lending rate to increase from its current setting of 0.25% to 1.25% by the end of 2022 in a series of hikes.

The Royal Bank of Canada predicts 2022 home sales to increase 19.8% from a year earlier, with the average home price increasing 3.3%. “We expect extremely tight demand-supply conditions will keep prices under intense upward pressure in the near term though we see such pressure easing significantly by the second half of 2022 as markets achieve a better balance.”

The Toronto Dominion Bank is forecasting a 7% increase in home prices this year, noting, “both new and resale markets remain drum-tight, suggesting another strong year for price growth is in the cards for 2022.”

The Canadian Imperial Bank of Commerce (CIBC) is the outlier, cautioning that home sales could drop in 2022 and condos may be the only sector to see price growth.

“Overall, we expect sales to fall by 15% in 2022, relative to the elevated level seen in 2021—an environment that is consistent with a notable deceleration in home price inflation next year,” wrote CIBC economist Benjamin Tal. “This environment is also likely to impact the relative value of condos vs. a single-detached unit. Logic suggests that higher rates will channel more activity into the more affordable condo market, resulting in relative price outperformance in that market.”

Victoria rent prices are officially more expensive than Toronto’s.

January 8, 2022

GagliardiPhotography/Shutterstock

If renting in a big city like Vancouver or Toronto is too expensive, then you might want to look to a smaller city to get rent relief.

But you’d be hard-pressed to find it in Victoria, BC, because it just surpassed Toronto, Ontario, as the second most expensive city to rent across Canada.

According to a new rent report from liv.rent, it’s a new year, with new higher rental averages for Victoria.

While Toronto used to be the most expensive city to rent in across Canada, Vancouver surpassed it in the summer of 2021.

Now, Victoria’s rental averages have risen enough to bump Toronto down the list again.

In Vancouver and Victoria, the average rent for an unfurnished one-bedroom unit is more than $1,800. Meanwhile, the same kind of unit in Toronto is much cheaper at $1,678 per month on average.

Vancouver rent has been climbing in the last six months, reaching a high in December at $1,831.

According to the Canada Mortgage and Housing Corporation’s 2020 data, the vacancy rate in Victoria is 2.2%.

It increased as the “COVID-19 pandemic slowed down demand growth,” said CMHC.

CMHC also said that rent in the city increased faster than inflation and the provincially allowable rent increase. The city continues to see rental affordability as a challenge, particularly for low-income households that need family-friendly units.

New aquatic centre a chance for Ottawa to make a splash, advocates say.

Would support athletes and attract major events, advocates say

January 10, 2022The City of Ottawa acknowledges its lone Olympic-sized, 50-metre swimming pool at the Nepean Sportsplex, seen here in 2017, has fallen behind the standards for international competition. That’s why it’s now seeking partners for a new aquatic facility. (Kate Porter/CBC)

Competitive swimmers in Ottawa haven’t been able to get home-pool advantage in a major competition for years.

If a big meet is held at the Toronto Pan Am Sports Centre, for instance, their southern Ontario rivals will know how the pool works and will have a routine and a home-cooked meal ahead of a race that could be decided by milliseconds.

That’s why a planned aquatic sport centre for Ottawa with one or two Olympic-sized 50-metre pools is being heralded as a welcome investment.

“It’s definitely something that would be nice to have. [You’d] get to sleep in your own bed and then race your best race the next morning,” said Alexandre Perreault, who competes with the University of Ottawa and the Ottawa Swim Club and is a former member of the national team.

The city is looking for partners for the aquatic centre project, with the aim of hosting large competitions within the next 10 years.

The deadline for expressions of interest is Jan. 14, less than one week away.

A new facility would help Ottawa’s swimmers ‘race [their] best race,’ said Alexandre Perreault, seen here at a 2018 competition in China. (Ng Han Guan/The Associated Press)

The local aquatic sports community has been calling for an upgrade to the city’s existing pools for some time, as Ottawa’s only Olympic-sized 50-metre pool, located at the Nepean Sportsplex, has fallen behind international standards after almost 50 years of operation.

That’s disqualified the nation’s capital from hosting major competitions.

“[A new centre] would give the younger generation in Ottawa an opportunity to have access to a better pool, better starting blocks, better air quality,” Perreault said.

Demand on pools ‘just huge’

There’s impatience for the project to get off the ground after Canada’s recent high-profile successes, said Marcia Morris, president of the Ottawa Sport Council.

“Swimming, because of what’s happening in the Olympics, is just becoming more and more popular. And the demand on our pools is just huge,” she said.

Hosting competitions also attracts tourism dollars, Morris said. While the new facility should be able to accommodate an event like the Canada Games, she said it also needs to provide opportunities to local athletes.

Along with encouraging athletes and drawing visitors to the city, an aquatic facility will also provide an opportunity to address the city’s overbooked swimming classes, said Rideau-Vanier Coun. Mathieu Fleury, the city’s sports commissioner.

Fleury said the city has set aside money for the construction of an Olympic-sized pool and has the expertise to run the facility, but other elements — and the funding needed to build them — will be part of the proposal process.

“It can’t just be a local pool, it can’t just be a hosting pool,” said Fleury.

“I think to get the projects that everyone wants — the local swimmers want and the hosting potential of that facility — we need to bring partners together.”

Carleton University, the University of Ottawa and the RA Centre have all expressed some interest in an aquatic sports complex in the past, the councillor said.

So has Peter Lawrence, a longtime leader in the water polo community who’s been working with various partners for almost half a decade to establish what he calls a “world-class” national aquatic complex in the capital region.

Their group’s project is even more ambitious than what the city’s laid out, as it may include a third Olympic-sized pool, a dedicated diving tank and even courts for basketball and pickleball.

From left to right, Canada’s Kayla Sanchez, Maggie Mac Neil, Rebecca Smith and Penny Oleksiak celebrate their silver medal at the Tokyo Olympics. Canada’s recent high-profile successes in the pool has made swimming increasingly popular, according to Marcia Morris, president of the Ottawa Sport Council. (Frank Gunn/The Canadian Press)

The estimated cost would be $300 million, and Lawrence said his group has designs on it being located on the federally-owned Hurdman lands. He said while the community would have access to the 24-hour facility, it’s also meant to retain athletes who’ve had to move or commute to Toronto to pursue their careers.

“We can’t have that. We’re destroying the potential for Ottawa’s high performance community. We really must provide facilities,” he said.

The city’s document for the new aquatic centre doesn’t lay out a specific location, although it does note a parcel has been identified in Riverside South for some kind of recreation centre.

It also says the project should be developed close to either LRT or bus rapid transit.

The Next Generation in Canadian Housing: Generation Z Trends Report.

December 8, 2021

According to a new generational trends report recently released by Mustel Group and Sotheby’s International Realty Canada, the Canadian real estate market is set to absorb an influx in demand as the next generation of homebuyers, Generation Z, is primed for first-time home ownership despite challenges with housing affordability.

Survey results revealed that 75% of urban Generation Z adults are likely to buy and own a primary residence in their lifetime, with 49% stating that they are “very likely” to do so; in fact, 11% already own their home. Despite high demand, 82% of those who have not yet purchased their first home are worried that they will not be able to do so in their community of choice because of rising housing prices, with 38% indicating that they are “very worried”. The top financial barrier to saving money for a down payment is paying for current living expenses, which was cited by 28%.

Despite these challenges, the desire to own a single family home remains high amongst this cohort, with 70% reporting that they would want to purchase a single family home in their peak earning years if budget were not a consideration. 13% and 11% say they would prefer to buy a condominium or attached home. Although 50% have already given up on their dream of owning a single family home, with 34% stating that they have given up due to the high cost. As a result, approximately half of those surveyed state that their most likely and realistic first home purchase will be a higher-density housing type: 25% report that their first home purchase will likely be a condominium, 18% say that their first home will be an attached home/townhouse and 7% state that their first home purchase will be a duplex/triplex. 39% report that they are most likely to buy a single family home as their first residence.

The Mustel Group and Sotheby’s International Realty Canada report is the country’s first in-depth study of the housing intentions, aspirations and preferences of Generation Z, a demographic that despite varying definitions of its current age bracket, has been defined by Statistics Canada as those born between 1993 and 2011. The first in a multi-report series revealing the survey’s in-depth findings, “The Next Generation in Canadian Housing: Generation Z Trends Report” is based on a survey of 1,502 Generation Z Canadians who are over the age of majority and between the ages of 18 and 28 in the Vancouver, Calgary, Toronto and Montreal Census Metropolitan Areas.

The report reveals differences in Gen Z’s sentiments, goals, and inclinations between Canada’s four largest metropolitan areas: Vancouver, Calgary, Toronto and Montreal.

*Disclaimer

The information contained in this report references survey results, plus market data from MLS boards across Canada. Sotheby’s International Realty Canada cautions that MLS market data can be useful in establishing trends over time but does not indicate actual prices in widely divergent neighborhoods or account for price differentials within local markets. This report is published for general information only and not to be relied upon in any way. Although high standards have been used in the preparation of the information and analysis presented in this report, no responsibility or liability whatsoever can be accepted by Sotheby’s International Realty Canada, Sotheby’s International Realty Affiliates or Mustel Group for any loss or damage resulting from any use of, reliance on, or reference to the contents of this document.

National Bank Of Canada Calls 2022 “The Year Of The Hike,” Sees Rates 6x Higher.

One of Canada’s “Big Six” banks is declaring next year to be “The Year of The Hike.” National Bank of Canada (NBC) chief strategist (and poet-in-residence) Warren Lovely is calling the first interest rate hike in just a few months. He sees the Bank of Canada (BoC) making its hike in March, way ahead of schedule. Over the next year, the overnight rate is forecast to recoup much of the ground lost during the pandemic. However, Canada’s real estate bubble will prevent it from going much further. Since the country went all-in on housing, it can’t pursue more aggressive policies like healthier economies.

The Bank Of Canada Will Hike Rates In March

Canada is expected to wind up its overly easy monetary policy pretty fast. Next year, National Bank sees five full, 0.25 basis point (bp) hikes. The first will be in March, bringing the overnight rate to 0.50% about a month before the BoC forecast. The only other institution to call a hike that early is BMO. However, mounting inflation pressures might force others to adjust in the coming weeks.

The remaining four hikes to the BoC’s overnight rate are forecast throughout the year. The second and fourth quarters are expected to see one full 0.25 bp hike each. In the third quarter, they see two full hikes. Canadians should see the overnight rate at 1.50% in one year, 6x the current level. That’s going to be a significant change.

Canada’s Real Estate Bubble Will Prevent Rates From Rising Too Fast

In 2023, they don’t see much more happening due to Canada’s real estate bubble. The bank only sees one more rate hike, topping out the country at 1.75% — the lower bound for the neutral rate. A neutral rate is the level of interest where money is cheap enough to support full employment but high enough to control inflation. According to the BoC’s last estimate, the neutral rate for Canada is between 1.75% to 2.75%.

The reason NBC only sees the rate rising to the lower bound is “interest-sensitive demand in the economy.” It’s a friendly way of calling out Canada’s real estate bubble, which is now so big it weighs policy decisions. “We don’t see the BoC as wanting to crush one of the main drivers of Canadian economic activity,” said Warren.

National Bank sees interest rates rising earlier than most other forecasts but ending faster. For example, Scotiabank sees interest rates climbing in the second half of next year. However, they also see rates rising closer to the middle of the neutral range, ending hikes around 2.25% in 2023. A slower start but higher rise compared to the NBC forecast.

While National Bank’s forecast is lower, it’s higher than the current rate, and that’s going to throttle credit. The forecast is the same level before the recession began, which had slowed home sales. It wasn’t until the end of 2019 when the BoC began providing mortgage liquidity injections, that the market picked up.

Bank of Canada to maintain current inflation mandate.

ByJordan Press (The Canadian Press)

December 13, 2021

Canada’s central bank will aim to keep the annual pace of price gains at its historic target rate, but will now more formally take into account the health of the job market as part of its inflation-targeting regime.

A new framework agreement between the federal government and the Bank of Canada announced Monday keeps at its heart a two-per-cent annual inflation rate.However, the central bank will now also consider employment levels and how close they are to the highest level they can reach before fuelling inflation when setting its trendsetting interest rate.

Bank of Canada governor Tiff Macklem and Finance Minister Chrystia Freeland stressed there was no material change to the bank’s marching orders, and that the consideration of employment does not constitute a dual mandate to hit two different targets — a measure that was under consideration for the mandate.The two framed the agreement as codifying the Bank of Canada’s interest in a healthy labour market, something the bank has stressed during the pandemic in explaining its moves.

“Monetary policy works better when people understand it,” Macklem said, “and, really, this agreement clarifies our objectives and it clarifies how we have and can use the flexibility that is built into our framework.”

Under the new agreement, the Bank of Canada may decide to allow inflation to sit closer to either end of the bank’s target range of one to three per cent for short bursts as it determines when the labour market hits its full potential.

It also has flexibility to keep its key interest rate at the lowest level possible for longer stretches to help the economy recover from a downturn.

Since 1991, the Bank of Canada has targeted an annual inflation rate of between one and three per cent, often landing in a sweet spot at two per cent.

Even under those previous mandates, the health of the labour market was a factor in decisions about whether to lower or raise rates, said BMO director of Canadian rates Benjamin Reitzes.

“Case in point, inflation is near five per cent and slack in the labour market has been a key reason why the (Bank of Canada) has kept policy rates at the lower bound,” he wrote in a note.

The Bank of Canada’s key policy rate since the start of the pandemic has been at 0.25 per cent, lowered there to prod spending during the COVID-19 induced downturn and subsequent rebound. As it stands, the bank doesn’t see a rate bump until April 2022 at the earliest.

Changes in the Bank of Canada’s target for the overnight rate influence the prime rates at the country’s big banks that are used as a benchmark for loans such as variable rate mortgages and home equity lines of credit. Changes in the rate may also influence bond yields, which can lead to changes in fixed rate mortgages and other borrowing.

Under the agreement Monday, the central bank said the rate may more often hit rock-bottom and remain there for longer if the bank believes it will help get inflation back on target.

A low-for-longer rate environment may sometimes be needed, the bank said, even if it boosts the likelihood that inflation could overshoot the two per cent target as the economy recovers.

Rate hikes could be more gradual than in the past as the bank figures out if it has properly estimated the full potential of the labour market, meaning that inflation could again rise above the bank’s target.

“This is one reason to think that inflation will, on average, be higher in the coming years than in the past decade, albeit not dramatically so,” said Stephen Brown, senior Canada economist with Capital Economics, noting inflation has averaged 1.7 per cent since the global financial crisis.

The bank noted that figuring out when the country has hit “maximum sustainable employment” may be “impossible” because it can’t be nailed down to one number, and is complicated by a greying workforce and increased digitization.

The bank plans to outline what labour market markers it is monitoring and detail those as part of its regular interest rate announcements.

The deal also outlines how the bank should consider climate change in its policies, although leaving it up to governments to hit emissions targets. “Monetary policy cannot directly tackle the threats posed by climate change,” the statement reads, latter adding that economic modelling should account for its affect on the financial system.

Alex Speers-Roesch with Greenpeace said that on the contrary, central bank policy can assist in fighting climate change. He pointed to the option of the bank buying more environmentally friendly assets, which the Bank of Canada is considering.

BC Real Estate Poised to Have Another White-Hot Year in 2022.

December 7, 2021

The Vancouver real estate market is slated for a white-hot year in 2022, following this year’s frenetic activity, says the President of BakerWest.

“I base this on substantial statistics,” Jacky Chan told STOREYS, “which our Minister of Immigration, Refugees and Citizenship rolled out that show we’re on track to accepting over 400,000 new immigrants or permanent residency applicants into Canada. In 2022, we’re on track to exceed that number with a 411,000 target. We’re talking about over 400,000 people coming into Canada annually over the next five years, which equates to around two million.”

Vancouver, the country’s third-largest city and one of its main beneficiaries of immigration — as evidenced by local job creation and, of course, the city’s housing market — is the most expensive in Canada. Demand for the city’s housing has vastly outpaced resale availabilities and developers’ abilities to provide new supply commensurately.

The Pacific Rim city is a leading destination for arrivals from across Asia in addition to Europeans and Americans, especially as the satellite offices spill out of Silicon Valley and up the coast. Chan says the cost of hiring qualified programmers and engineers in Vancouver is 30-35% lower than it is in Silicon Valley, and he added that, while major Canadian cities are often rebuked for having unfavourable tax regimes, the overhead in a city like Vancouver makes more financial sense than it does in the Golden State, which explains the enthusiasm with which Amazon, Facebook, Google and Shopify, to name a few tech juggernauts, are opening offices in the city.

To explain the surge of activity Chan forecasts for Vancouver’s real estate market in 2022, he advises analyzing the current preconstruction condo market.

“With preconstruction sales this year, we’ve seen massive towers of 300-450 units sold out in a single day, so demand is definitely there even though supply is always not enough, therefore, prices have to go up,” he said. “The preconstruction market in 2022 will be very strong because of the lack of inventory in the real estate market, which discourages conventional offerings as well as the ability to purchase existing properties, of which there aren’t enough on the market to begin with, because you’re fighting with 20-30 people for one home, whereas, through preconstruction sales and marketing, we’re focused on selling entire projects with a minimum of 20-30 units all the way up to 500-plus units, and when we do that it is way easier to service demand for a multitude of people at the same time. The reason is that developers and marketing agencies can gauge and arrange the allocation for buyers. For example, if a particular floor plan of unit A is not available on the 10th floor, we can offset that demand and offer the same floor plan to the same client on the ninth or 11th floor, and that satisfies their demand.”

Underpinning continued, if not stronger, preconstruction condo demand in 2022 is less buyer competition, which keeps prices in check as opposed to bidding against 20-30 other desperate buyers for a scarce low-rise dwelling.

In the second half of this year, condo developers were confident enough to launch new projects in Vancouver, reasoning that the worst of the COVID-19 pandemic is in the rear-view mirror, and absorption has been robust enough to ensure launches continue through next year.

“In some cases with the projects we oversaw at BakerWest, some were sold out within the first month, and all of them were sold out in a two- to three-month period, and this trend will definitely continue as there isn’t enough supply,” Chan said, adding that could change depending on the area. “Vancouver, its downtown, north shore, Richmond and the Fraser Valley service different purposes, and different price points exist in different municipalities.”

Indeed, the multiplicity of municipalities reflects a variance of demand cycles. From Abbotsford to the Tri-Cities — Coquitlam, Port Coquitlam, Port Moody, and the villages of Anmore and Belcarra — supply is lagging far behind demand, Jamie Squires, Senior Vice President and Managing Broker of Fifth Avenue Real Estate Marketing, says.

“In every region, there’s been extremely high demand and a lack of supply, and there are only a handful of certain types of listings, depending on which neighbourhood you want to be in. Where you used to have 50-100 townhomes, now you only have five listings and people to compete with, which I don’t see changing much,” she said. “Once projects come through municipal approvals and they launch, they sell out in a month, some even in a day — although we try not to do that because we feel we haven’t worked in our clients’ best interests if we do that.”

New build presales have spiked in Surrey City and North Delta with 2,543 high-rise sales, 1,071 low-rise sales, and 626 new townhouse sales. Squires noted that few immigrants have arrived in Canada during the pandemic, yet sales have been persistently elevated because, in addition to buyers within the province, BC real estate has gotten a lot of attention from purchasers wanting to flee dreaded Prairie winters. And as the pandemic appears to be waning and more newcomers start arriving in the country, demand is set to arise again in 2022, albeit by only 2-3%, Squires estimates.

“The biggest issue now is a clear lack of supply, so as long as the government does something to push cities and municipalities to be more accountable to approval times, I don’t see a huge influx of supply happening to stabilize this market,” she said.

Kelowna is experiencing unprecedented presale absorption, according to Scott Brown, Development and Marketing Lead for BC at Peerage Realty Partners West, because, unlike in the aftermath of the Great Recession when urban cores generally rebounded before suburbs, the coronavirus has created conditions for an obverse recovery this time around.

“In Kelowna, Victoria, and you could argue Kamloops is a third, prices have gone up significantly,” Brown said, ”but you could still find a wood frame project in downtown Kelowna for $600-800 per square foot. Kelowna is attractive to younger and older people moving out of Vancouver because they’re getting price appreciation there. Langford, Kelowna, Greater Victoria and the Okanagan are driven by the exodus of higher density areas of BC, like Vancouver, and the older buyers want to live in smaller, less busy cities, while a significant amount of young people are flexible with their work arrangements and are choosing to enter those markets because they can still afford a home and work remotely.”

As a result, Brown anticipates 2022 will be a very strong year for home sales in the province, although perhaps the pace won’t be as torrid as has been in 2021. Brown also believes the rapid pace of appreciation will stabilize by next year, but if it exceeds this year’s pace, it will not be by much.

“It will either be a little over or a little less because of the chronic undersupply.”

Victoria has one of Canada’s most expensive real estate markets, and although sales declined by 24.7% year-over-year in October, it doesn’t tell the whole story. According to internal data from The Condo Group, demand has continued growing which means that a new-listings dearth is the likely reason and it will most likely persist into 2022.

“The local municipalities are under a great deal of public pressure to expedite the approval process for multifamily projects moving forward, however, even if every project that is going through the approval process gets approved, it can still take a long time for buildings to complete,” Tony Zarsadias, President of The Condo Group, said. “Despite challenges in the resale market, the market for new, presale condominiums and townhomes remains equally strong and developers are doing their best to add more inventory. There are solutions out there.”

The appetite for new homes in Victoria is so strong that The Condo Group sold out the first phase of a townhome development in the Tillicum area without the help of a show room. As a result of buyer fatigue in the resale market, Zarsadias anticipates even more growth in the market’s new build segment.

“Many hopeful homebuyers have been losing out amid multiple offers over 2020 and 2021,” he said. “With that said, the seemingly imminent increase in interest rates is keeping buyers focused on making a move to take advantage of the historically low interest rates we’ve seen over the past two years. As we’ve seen historically, when rates start to go up, we typically see buyers take a temporary break, reset, reevaluate, and then get back into buying mode with renewed focus.”

The Great Canadian Restart: How 2022 can spark an era of greener, more robust growth.

If 2021 was the year Canada rounded the corner on the pandemic recession, 2022 is the year it can accelerate out of a decades-long pattern of slowing growth.

Though a pandemic recovery is in sight, a slow-growing labor pool and lackluster record on investment and innovation have set a low-speed limit for the economy.

The greener, more digital, and tech-enabled society accelerated by COVID-19 has opened new pathways for growth that could ignite spending, investment, and innovation. Businesses and households are lined up to propel this change, but their efforts are likely to be hampered by near and long-standing obstacles.

As it starts its new mandate, the federal government can help set a new course. Growth-oriented federal and provincial government policies can be the foundation for the increased private investment needed to boost Canada’s growth trajectory.

Other countries are already remaking their economies in a bid to reverse the secular trend of low and declining economic growth rates. Canada does not want to be left behind. With a skilled workforce, strong record as a tech and energy innovator, and investment opportunities, it doesn’t have to be.

Source: Statistics Canada, Haver, RBC Economics

A 6 point plan for growth

1. Embrace new approaches to innovation policy

2. Forward-looking policy, public infrastructure and blended finance for climate action

3. Promote services trade and Canadian platforms; protect intellectual property and data

4. Increase competitiveness with tax, competition, and regulatory policy

5. Attract, develop and retain new sources of talent

6. Education and labour market policy for lifelong learning

Back to the starting line

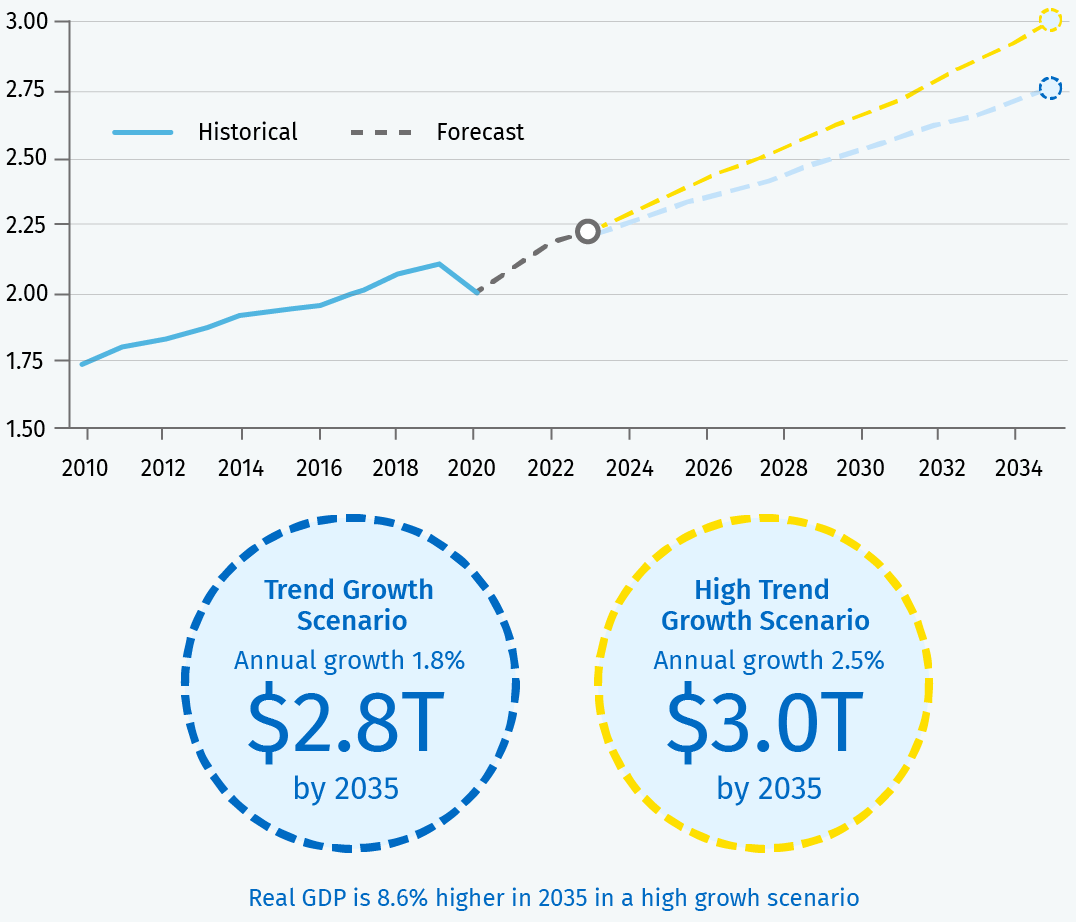

GDP remains down compared to pre-pandemic levels, due to some particularly weak sectors. But many areas of the economy have already recovered or surpassed pre-pandemic levels. A mix of consumer spending approaching pre-pandemic levels, strong investment intentions, billions in business and household savings, and a supportive external environment will help fuel the ongoing recovery in 2022, even as firms continue to struggle with supply chain disruptions and a labour crunch. RBC forecasts growth of 4.7% in 2021, declining to 4.3% in 2022 and 2.6% in 2023 as it converges to its long-term trend1.

With the end of the recovery—or cyclical growth—nearly upon us, we face a new question. Following the once in a century shock of the pandemic, how can we build more robust growth into Canada’s economy?

Over five decades, the country’s growth has been anything but dynamic. Real economic growth rates fell from an average of 4.1% in the 1970s to 2.1% between 2010 and 2019. Should we carry on our existing course, we expect a return to a sluggish trend growth of around 1.8% per year beyond 2023, a record reflective of slow labour force growth and muted productivity.

Canada isn’t alone. Many other advanced economies have experienced the same deceleration, attributed to a greying population, the slowing pace of innovation, and in some cases, post-recessionary economic scarring. The trend has been stubborn, suggesting that underlying structural issues will continue to be a powerful force now and into the future.

A new set of starting blocks

The next decade can be different. But if Canada is to secure a new growth trajectory, the private sector must take the lead. With an increase of $200 billion in the value of liquid assets since the start of the pandemic—and with long-term interest rates still low—corporate Canada has the muscle to do it.

There’s a business case for investment. Consumer surveys show a continued desire to engage with e-commerce. Canadians want to shop in a responsible way that favours local businesses and respects the climate and how employees are treated. And intensifying labour shortages provide a good reason to make production more efficient through new investments in automation and equipment.

Businesses’ investment intentions are up in recent surveys, with a majority saying capital expenditures over the next two to three years will be higher than before the pandemic. Many are focusing on digital investments.

It’s still too early to see a surge in business investment, but early evidence is encouraging: machinery and equipment (M&E) investment is above 2019 levels (excluding transportation equipment). Investments in research and development (R&D) and software are up, too. Trade data show a recovery in industrial machinery imports and a rise in imports of electronic and electrical equipment.

Increased digitization and automation should boost productivity, data and product development. And digitization—together with a greying population that tends to consume more services—can create opportunities for expanded services trade. Investment is needed for decarbonization, mitigation, and development of new green technologies. These same shifts in the global economy can bring opportunities for Canadian firms to export products and expertise, earning global incomes that can help fund the domestic adjustment to the new economy—one with greater spending, investment, innovation and growth.

Getting there will mean tackling new economy challenges, including changing sources of economic value that risk capital obsolescence and loss of competitiveness. It will mean responding to shifts in skills and jobs that threaten displaced workers, and inequality. It will also mean reckoning with where we have not performed well in the past.

Switching leads: Confronting a poor record on business investment and innovation

To achieve a materially different growth outlook, Canada needs to see a big shift in actual business investment and innovation.

Canada has a longstanding investment gap with peer economies. The C.D. Howe Institute finds that Canadian non-residential business investment per worker has lagged behind the U.S. since at least 1991 with the gap widening through the 90s, the mid-2010s and then again during the pandemic. By the second quarter of 2021, Canadian businesses invested 50 cents per worker for every dollar in the U.S3.

The driver of Canada’s mid-decade underperformance was investment declines in the oil and gas sector shortly after the 2014 oil price shock. This investment, which is concentrated in non-residential structures, fell about 60% from its peak prior to the pandemic and remains weak. For the rest of the economy, the Canada-US investment gap stayed relatively stable, but the absolute gap is particularly high.

Canada has also seen a widening investment gap with the U.S. in machinery and equipment (M&E) and intellectual property (IP), driven in part by the oil and gas sector, but also weak M&E investment in other sectors. Investment in both M&E and IP stopped growing as a share of the economy after the Global Financial Crisis (GFC).

Canada has seen a declining GDP share of business investment in research and development, in contrast to many other OECD economies that have seen growing shares.

Given the lag in business investment, it’s not surprising that Canada has a labour productivity gap with the U.S. While the gap narrowed slightly post-GFC, by 2019, Canada produced just 74 cents per hour worked for every $1 in the U.S.

Meantime, lagging innovation could soon present an even greater problem. As technology advances, more economic value will be encapsulated in data, algorithms, brands, digital services and other ‘intangible assets’. With these assets being more scalable compared to tangible inputs like physical capital and labour, delivering large gains to its developers and owners, economic prosperity will increasingly depend on our transition to an innovation economy. And while innovation and competitiveness are influenced by many factors, from policy and demographics to the external environment, business investment is essential.

To varying degrees, Canada performs well in international rankings for entrepreneurial ambition, market sophistication, venture capital financing, institutions, and a skilled workforce. But it ranks poorly in other innovation inputs, with low business R&D investment, low adoption of information communications technology, low per capita scientific activity, an inadequate IP regime, and low openness to competition. And Canada has had trouble translating inputs to innovation outputs. It has middling patent activity, low business creation, and difficulty scaling businesses into global exporters. Firms that are able to export globally are a signal of economic competitiveness, yet net exports have been a drag on economic growth in Canada for much of the past two decades.

The result is imbalanced economic growth. When balanced, growth is derived from multiple sectors of the economy—consumption, investment, and net exports. For Canada, the imbalance between the low growth contribution from net exports and business investment on one side versus high contributions from consumption and housing on the other, means the economy is more exposed to individual economic shocks. For example, a shock to the housing sector could directly reduce economic growth through less construction and sales, and potentially force an abrupt, costly reallocation of resources to other sectors. With climate actions and trade tensions darkening prospects for Canada’s biggest export—crude oil—this imbalance could get worse.

New hurdles: Canada’s climate challenge

In addition to long-standing challenges, there are newer obstacles to unleashing spending and investment.

For one, firms that are trying to manage with higher pandemic debt levels, supplier challenges and labour shortages may struggle to plan for the future. Small businesses have historically lagged behind in digital adoption and the pandemic has further burdened seven in 10 of them with additional debt loads averaging $170,000.

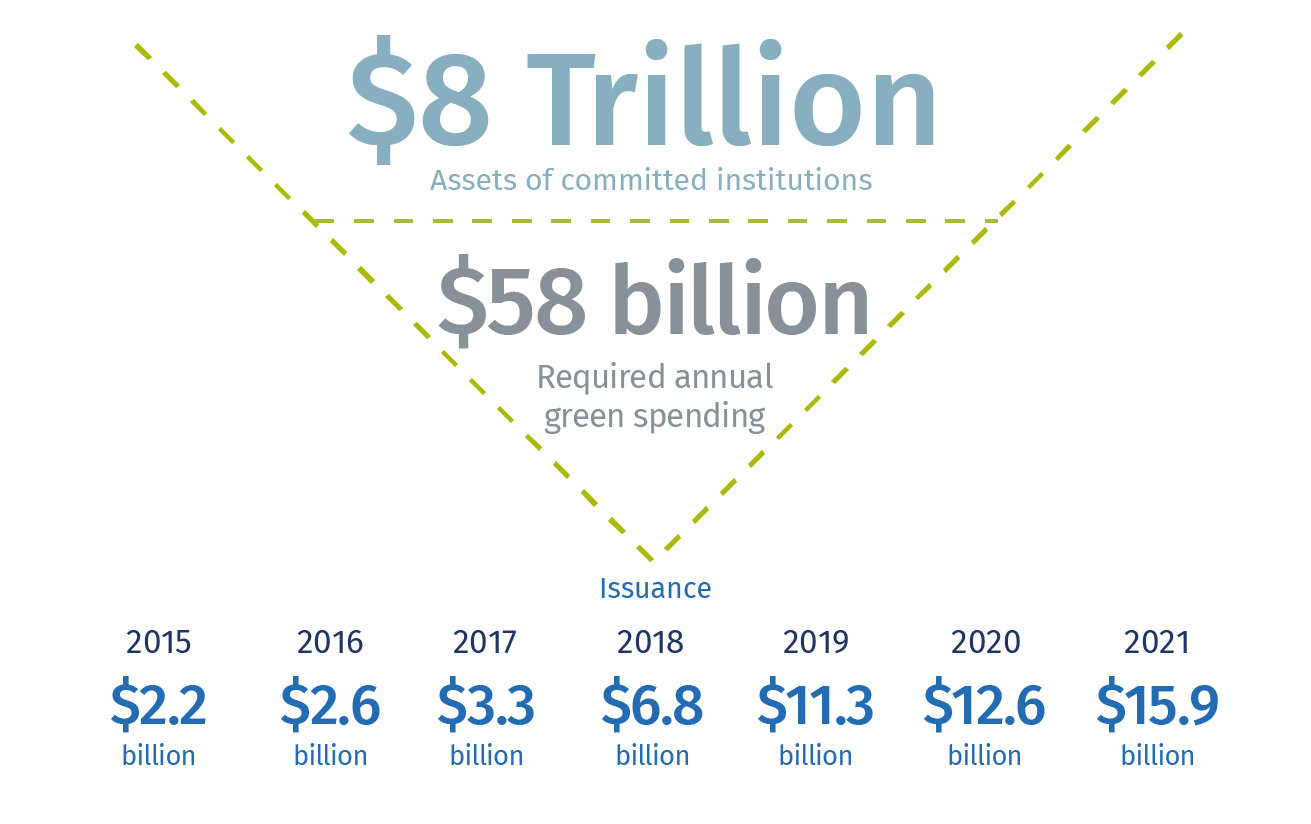

There are also impediments to connecting huge climate funding commitments to green projects. Large Canadian firms with $8 trillion in global assets have committed to Net Zero by 2050, yet spending on green projects is still much lower than the $60 billion per year we estimate that Canada needs to reach.

Only 6% of Canadian firms plan to measure their environmental footprint over the next year, including less than 25% of large firms with 100+ employees.

And while the pandemic, a lack of financial resources, and clients not willing to pay a higher price are sometimes identified as hurdles to adopting green practices, the majority of businesses identified no challenges.

Source: Bloomberg, RBC Economics | *data to November 1, 2021

The outcome for growth will also depend on supply. If the supply of finance is not a challenge, the availability of some goods may be. As much of the global economy edges toward a green, digital and tech-equipped society, there will be greater demand for the goods that facilitate it—5G networks and cybersecurity systems, critical minerals, batteries, EVs, and renewables. Meeting this demand will take time. Semiconductor factories and lithium mines can take a decade to develop. And the increasingly nationalist agendas pursued by many countries may reduce access to these competitive resources.

Yet it’s another, more localized supply constraint that may pose the most significant challenges.

The lynchpin: Human capital

Canada needs people and skills to reshape the economy. But population ageing and the changing nature of work threaten disruptions in labour markets that could become a significant drag on growth. These are not future problems. The economy was already grappling with labour shortages that have only been accelerated by the COVID-19 crisis. Pandemic-delayed retirements have created a potential wave of workforce exits in the year ahead and immigration levels have still not recovered. This is reflected in a third of businesses reporting labour shortages and a high national job vacancy rate of 6%.

These labour shortages will intensify. Population ageing has led to a declining labour force participation rate, which has subtracted about 1 million people from the workforce since its peak, and represented a drag on economic growth since 2010, when the first baby boomers turned 65.

The participation rate is projected to decline further over the next 15 years and could mean an additional 1.5 million fewer workers over that period, including up to 600,000 over the next three years.

Higher government immigration targets, if met, would address the pandemic immigration shortfall and help boost the number of available workers. But it won’t be enough. To keep the age structure of the population constant at 2020 levels, the annual immigration targets would have to double.

Getting everyone in the race: Canada must tap its rich supply of human capital

Large pools of talent remain underutilized in Canada. Closing the women’s participation rate gap would add another 1.2 million people to the labour force. And other segments of the labour force have been underemployed relative to their credentials. Closing the visible minority earnings could lift GDP by nearly $30 billion per year7, and while not additive because of overlapping populations, closing the immigrant employment and wage gap has the potential to add $50 billion per year in GDP. Indigenous Canadians are also a significant source of untapped potential, particularly given they are the fastest growing youth population.

Having the right number of workers is key, but skills are just as important. If graduating youth are equipped with new skills and starting in new fields, the impact of potential displaced workers could be minimized. But some educational programs are not keeping pace with change, access to work integrated learning can be uneven, and young people can struggle to get hold of the information they need to make career choices. Despite greater demands, post-secondary institutions face a constrained funding model with tuition freezes and reliance on high-paying international students.

Mid-career workers face different challenges. While tight labour markets should incentivize more business spending on employee training, low wage workers whose jobs are more likely to be affected by automation, and who could benefit the most from upskilling, are also the least likely to participate in it.

Competing for the workforce of the future

A skilled labour force, world-class educational institutions, and an open immigration system give Canada an edge in the global race for talent. But Canada is not the only country struggling with an aging population. Other countries are also looking for highly-skilled immigrants to build their clean and knowledge-based economies.

International firms are using new remote work options to recruit international tech talent. Amazon, Google, Microsoft and Netflix have made plans to aggressively recruit in Canada this year. And while resident Canadians earning Silicon Valley wages may be good for the local economy, it could also be a growth-limiter for Canadian firms if they cannot compete in the international skilled labour market.

Canada’s high housing prices could be a challenge: about 60% of Canada’s permanent residents end up in Toronto, Vancouver, or Montreal, yet two out of three of these cities have among the highest housing costs in the world measured against median incomes9. House prices are even challenging for higher-earning workers. Remote work may help with this, but knowledge-based workers may still be drawn to cities.

Setting the course: The government needs a growth-oriented agenda

To avoid missing out on investment, innovation and talent, Canada must take a closer look at the overall policy framework. Specifically, structural policy—tax, regulation, competition, infrastructure, education, innovation, and trade policy—must work in concert with sectoral strategies and government spending programs to address the challenges before us.

Governments have spent a lot on income support and other programs since the start of the pandemic—an estimated additional ~$400 billion in program expenses over two years (a 50% increase) just at the federal level—preventing long-term scarring to labour markets and balance sheets. Now, their focus has turned to ‘recovery funding’ directed at still-struggling sectors and a range of economic and social issues. Some of this isn’t temporary. Governments have introduced major structural spending programs and, at least at the federal level, signs are any ‘fiscal space’ will be used to expand spending.

This doesn’t need to be a bad thing for economic growth. Social infrastructure like health care, community services and public housing enable individuals to participate in the economy. The pandemic helped shift the policy lens to varying health and economic outcomes, including longstanding equity gaps. Inequality, particularly at high levels, can impede economic growth through insufficient human capital development, weaker consumption or political instability.

And, there is greater recognition that more expansive fiscal policy could be important to breaking free from a low growth economy. Many economists believe that inadequate government spending held back the post-GFC recoveries in the U.S. and Europe. Given the relatively sanguine attitude of bond markets to high government deficits in advanced economies, and low interest rates, governments seem to have more fiscal firepower than they previously thought. Several global economies are experimenting with higher levels of deficit-financed public spending to spur spending, investment and growth.

But these relationships aren’t guaranteed, especially if social spending only finances current consumption, doesn’t target the largest equity gaps, or discourages employment. And financing government programs with a deficit comes with a risk: the new spending might not lead to sufficient economic growth to address future interest rate increases or other economic shocks.

Canada needs a focused, growth-oriented fiscal program to balance these risks. Targeted and forward-looking government policies can be the foundation for increased private investment that tilts Canada’s growth trajectory.

A six-point growth plan

The challenges may be clear, but the solutions are less so. Past policies have struggled to change the course. The increasingly green, knowledge and services-based economy could represent a new growth trajectory for Canada, but it needs a push.

There’s no single policy solution. Canada needs to confront the big challenges of the new economy, like climate policy, IP framework, and skills strategy, and realign the longstanding policy frameworks of the old one, including tax, competition and regulatory policy.

A growth-focused government strategy would encourage increased capital investment in technology and process innovation, helping Canadian firms scale to global markets. It would also enhance outcomes for Canadians in untapped talent pools, promote systems of lifelong learning, and support labour market transitions.

1. Embrace new approaches to innovation policy

Canada’s poor performance on business R&D investment has persisted in spite of above-average government support. Its approach to innovation—providing support through the tax system skewed heavily towards small and medium-sized firms—may be a barrier to innovation output and scale. Meantime, the U.S. and other countries are increasingly pursuing strategies to build economic capacity and compete for geopolitical dominance in new industries.10

Canada should test alternative innovation policies, including providing more support within core programs for larger, growth-oriented firms. More focused, de-politicized and resourced industrial strategies focusing on green and advanced technologies within North American supply chains may de-risk projects and draw private capital. Government procurement and targeted business supports may also accelerate technology adoption.

2. Forward-looking policy, public infrastructure and blended finance for climate action

The gap between green financing commitments and investments—and emissions targets and emissions—reflect a lack of projects with clear financial returns. Given the long time horizon, uncertainty is high around paths to decarbonization and underlying technology costs. Smaller markets for greener products mean firms may not be able to pass on abatement costs to their customers, challenging competitiveness for those that cut emissions.

Governments could prompt more climate action. Carbon pricing should continue to be a key pillar of the plan, rising predictably and applying more broadly. Hard infrastructure like EV-charging networks and carbon pipelines can help make it easier for households and firms to invest in emissions cuts. Canada should push for international cooperation on border carbon adjustments to protect domestic industry while furthering international progress on climate goals. Policy strategies can lay out a clear pathway for individual sectors, from oil and gas to agriculture, and promote blended finance pools of public, private and Indigenous capital for the early stage technologies we may need by 2050.

3. Promote services trade and Canadian platforms; protect intellectual property and data

Canada is a net exporter of R&D services and also a net importer of IP, suggesting Canada is not retaining ownership of its IP and is instead leasing it back from foreign companies. And foreign tech companies are monetizing Canadian data assets. With scalable, intangible assets driving tremendous value, this could be a missed opportunity to drive the scaling of Canadian firms and services exports. A broad range of services, from health care to software to the digital services embedded in the Internet-of-Things, are primed for growth.

Canada needs to consider forging trade agreements that address barriers to expanded global services trade. It needs to review its intellectual property regime to incentivize IP retention and outline data rights. Global platforms should be taxed at the same level as Canadian intermediaries, while multinationals should see time limits on tax benefits, with public money focused on local procurement over employment. Policy can support the development of Canadian platforms featuring local commerce, education and travel.

4. Increase competitiveness with tax, competition, and regulatory policy

Expectations of more public spending are raising concerns over future tax increases and creating uncertainty that may be limiting investment. Canada’s tax system has not been reviewed since 1967, and deviates in important ways from core tax policy principles like efficiency and simplicity. Canada’s low international rank in openness to foreign direct investment could be holding back innovation, while interprovincial trade barriers may be subtracting up to 3.8% from the economy per year. 11

Canada should undertake a tax policy review to streamline tax expenditures, ensure competitive rates of personal taxation (including for international skilled talent), encourage more public-private investment, incentivize re-investment and longer investment horizons, and target tax supports for newer and growth-oriented firms. Regulatory policy, especially in the context of interprovincial trade, also needs attention.

5. Attract, develop and retain new sources of talent

Affordable childcare and flexible working hours have long been identified as major barriers to women’s participation in the workforce. Meantime, challenges in integrating newcomers into labour markets, and opportunity gaps for Indigenous and some visible minority groups, have left other rich sources of workers underutilized.

National child care can have a big impact by targeting the largest affordability and accessibility gaps, while national standards within the early learning system can help expand the next generation of talent. Making the higher annual immigration target of ~1% population permanent, updating special visa programs with a more forward-looking assessment of labour market gaps, recognizing foreign credentials and providing greater pre-arrival labour market support can increase the participation of immigrants. Underrepresented groups should be encouraged to develop new green and digital skills.

And good housing market policy is good labour market policy. Governments of all levels need to coordinate a systematic review of housing policy to address supply-side constraints, rationalize demand-side policies, address inequality, and ensure financial and economic stability.

6. Education and labour market policy for lifelong learning

Despite a relatively high share of adults participating in on-the-job training, Canada has some of the largest participation gaps in the OECD.12 Workers who are highly-skilled, of prime-age (25 to 54 years) and employees of larger firms are most likely to get training.

Canada should explore redesigning income support programs to enable more reskilling while working. Policy makers should update the skills strategy and Canada Training Benefit for green skills and explore national tuition standards to balance access and revenue needs. Provinces should study rapid reskilling programs in various sectors to scale what works, accelerate the incorporation of skilled trades and digital and coding skills into their K-12 curriculums, and provide support for collaborative approaches and common platforms for helping small and medium-sized employers better prepare for their skill and training needs.

Canada’s immigration boost could fuel hot housing market: experts.

BySteve Scherer and Julie Gordon – December 9, 2021

Canada hopes more immigration can boost economic growth and allay a worsening post-pandemic labor shortage, but new migrants could pour gasoline on that red-hot housing market that the central bank has warned was stoked by “a sudden influx of investors.”

Prime Minister Justin Trudeau’s administration is on track to meet this year’s goal of 401,000 new permanent residents and is set to revise up next year’s target of 411,000, a government source said.